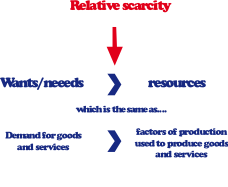

Relative scarcity

Economics is all about how economic agents (e.g. consumers, producers, governments, etc) make decisions about the use of resources (such as our land and labour) that exist in economies. These decisions must be made because every nation demands countless goods and services that require resources (or factors of production) to produce them. However, nation’s resources are limited when compared to the demands placed upon them. This creates an ‘imbalance’ that is referred to as the problem of relative scarcity.

Typically, our resources fall into four major categories:

- Land and natural resources (e.g. forests, minerals, water, etc.)

- Capital resources (e.g. machinery, robotics, trucks, etc.)

- Labour resources (e.g. workers such teachers, managers, etc.)

- Entrepreneurial resources (e.g. Gina Rinehart, Bill Gates, etc.)

All of these resources exist around us in various forms within our economy. They all have one important characteristic in common: they are all key inputs in the production process. Every business will have examples of all four ‘factors of production’ working to produce goods and/or services.

Given that all resources (which are relatively limited or scarce) can be valued by money, and all demands for goods and services are typically valued in monetary terms, scarcity also means that we don’t have enough money to purchase all of the goods or services that we desire. Accordingly, every one of us encounters the problem of relative scarcity every day. We must therefore make a choice about how we should best use our resources (or money) to satisfy our demand for goods and services.

Course notes quick navigation

1 Introductory concepts 2 Market mechanism 3 Elasticities 4 Market structures 5 Market failures 6 Macro economic activity/eco growth 7 Inflation 8 Employment & unemployment 9 External Stability 10 Income distribution 11.Factors affecting economy 12 Fiscal/Budgetary policy 13 Monetary Policy 14 Aggregate Supply Policies 15 The Policy Mix